Welcome to the Housing Market Trends November 2024 monthly update from Homes for Heroes. This report focuses on the residential real estate housing market. We listen to the experts and boil down what they have to say to assist you, our heroes, with decision making regarding buying a home, selling your home, or refinancing your mortgage.

Housing Market Trends November Key Takeaways

The housing market is ever-evolving. Economic factors, government policies, interest rates, and even socio-cultural shifts can play a role in how the market behaves. That said, here are some housing market trends for October to help keep you informed as you determine what’s best for you.

- Mortgage Rate Trends – Mortgage rates have been on the rise since the week of September 19, but the Fed cut the federal bps rate by another 0.25% on November 7th.

- Home Inventory Trends – Inventory continues to increase, and is likely having a direct impact on home prices.

- Home Pricing Trends – Home prices are continuing to appreciate year-over-year, and they are expected to continue appreciating, but at a slower rate into 2025.

- Save with Homes for Heroes – The Homes for Heroes program provides significant savings to community heroes, with an average savings of $3,000 after buying, selling, or refinancing a home with their local specialists. Sign up today to learn more and a member of the team will contact you.

Housing Market Trends November 2024 in Detail

Mortgage Rate Trends

The much anticipated meeting of the Federal Reserve took place on September 18th and as many predicted, the Fed reduced the federal funds target rate. This is not an interest rate, but it is a factor used in determining mortgage interest rates.

On September 18, 2024 the Fed reduced the federal funds target rate by 0.50%. On the following day, U.S. markets climbed to record highs.

Today, November 7, 2024, the Fed dropped the federal funds target rate another 25 basis points to a range of 4.50 – 4.75%. This is helpful news, and will hopefully influence mortgage rates enough to drop them over the coming months, considering mortgage interest rates have trended upward since the half-point drop implemented by the Fed in September.

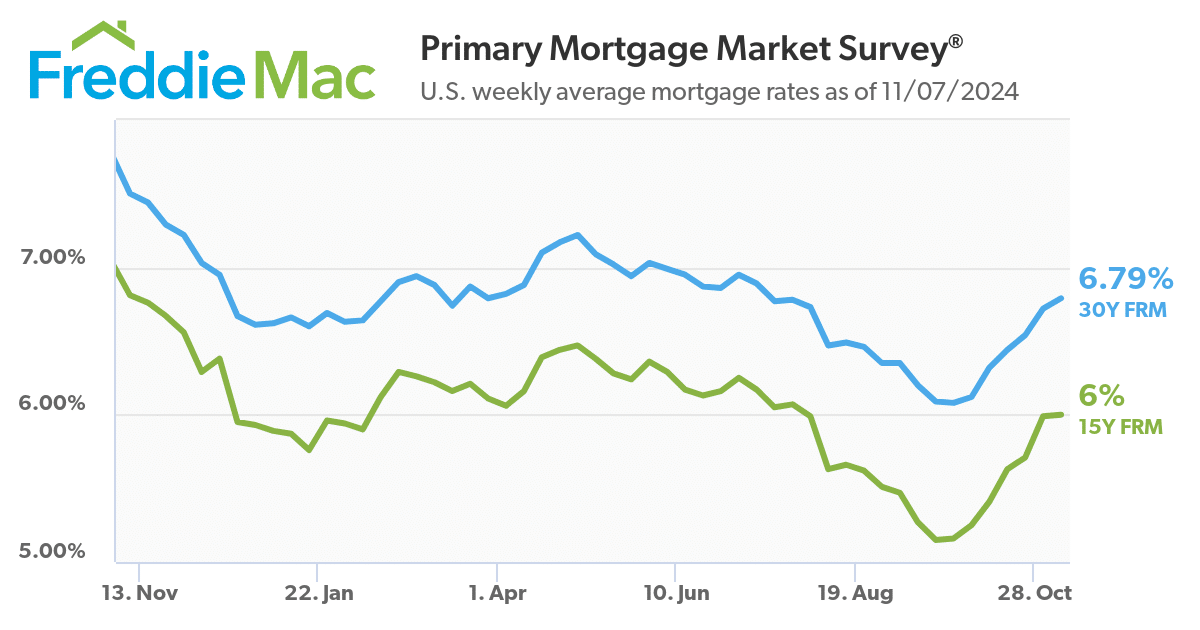

Freddie Mac’s Primary Mortgage Market Survey line graph above shows the increase in interest rates since the week of September 19, 2024. As of today, November 7th, the weekly 30-year fixed mortgage rate came in at 6.79% and the 15-year fixed mortgage rate landed at 6.00%. That’s an increase since September 19th, when the 30 year fixed mortgage rate was at 6.09% and the 15-year was at 5.15%.

The increase in mortgage interest rates over the past seven weeks, runs counter to what potential home buyers were hoping to see, following the rate reduction by the Fed. However, many industry experts have said most of the mortgage rate reduction happened pre-Fed announcement in anticipation of a rate reduction happening in September.

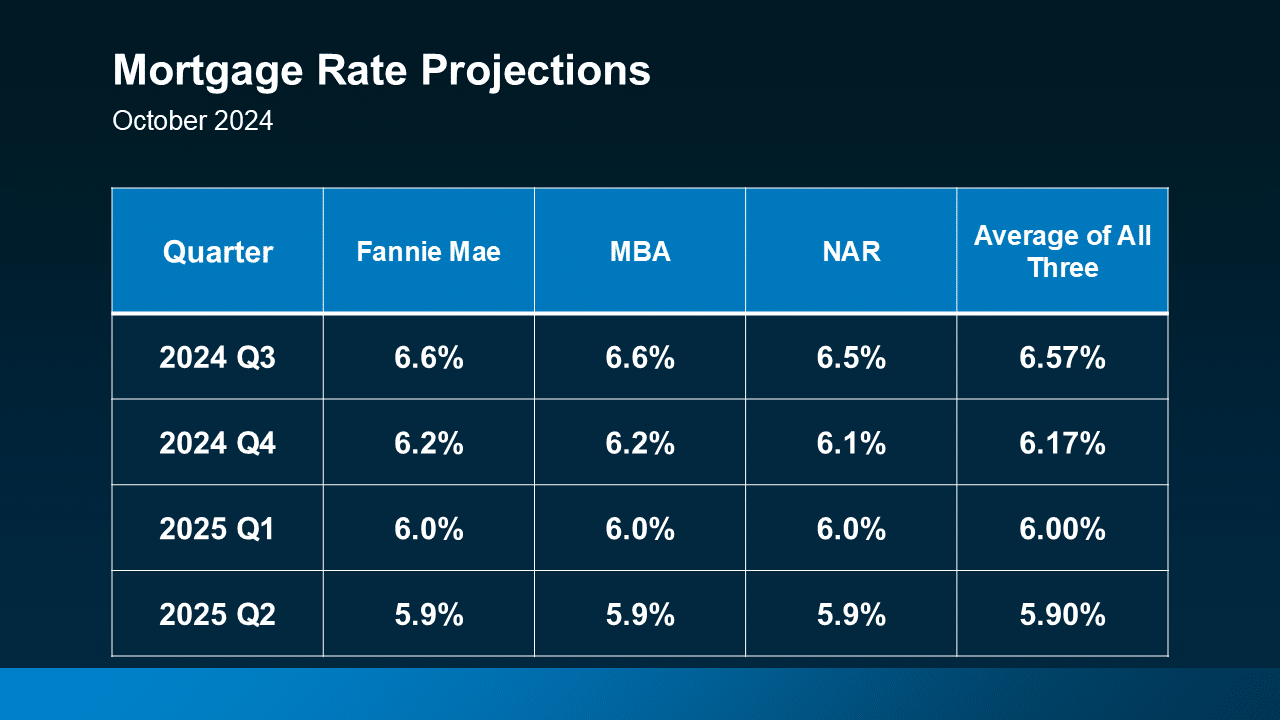

The mortgage interest rate trend is projected to decline over the next 6-9 months, but it is anticipated to be a much more gradual decline. The table above shows an average mortgage rate projection for Q4 2024 of 6.17%, and a trend that gradually declines, eventually landing on an average mortgage rate of 5.90% in Q2 2025.

There will be some ups and downs during this time frame, but the gradual decline in mortgage rates is what potential buyers need, especially given recent increases in mortgage rates.

Hopefully the additional rate reduction of 25 bps by the Fed today, and having the presidential election behind us, will help spur interest rates to start moving down again.

If you are thinking about getting into the housing market, remember to consider working with Homes for Heroes real estate and mortgage specialists to help you through the process. We will save local heroes (firefighters, EMS, law enforcement, military and veterans, healthcare professionals, and teachers) significant money when you close on a home with our specialists. On average you can save $3,000 if you buy a home, and $6,000 if you buy AND sell a home.

Sign up today and a member of our team will reach out to answer your questions, and to find out how we can best serve you.

Home Inventory Trends

The National Association of Realtors (NAR) reported the inventory of unsold existing homes increased 1.5% in September 2024, versus the previous month of August, continuing the increase in inventory trend this year.

More inventory of existing homes versus the previous month is good news, but there’s a long way to go, and this lack of inventory continues to affect home prices.

Home Pricing Trends

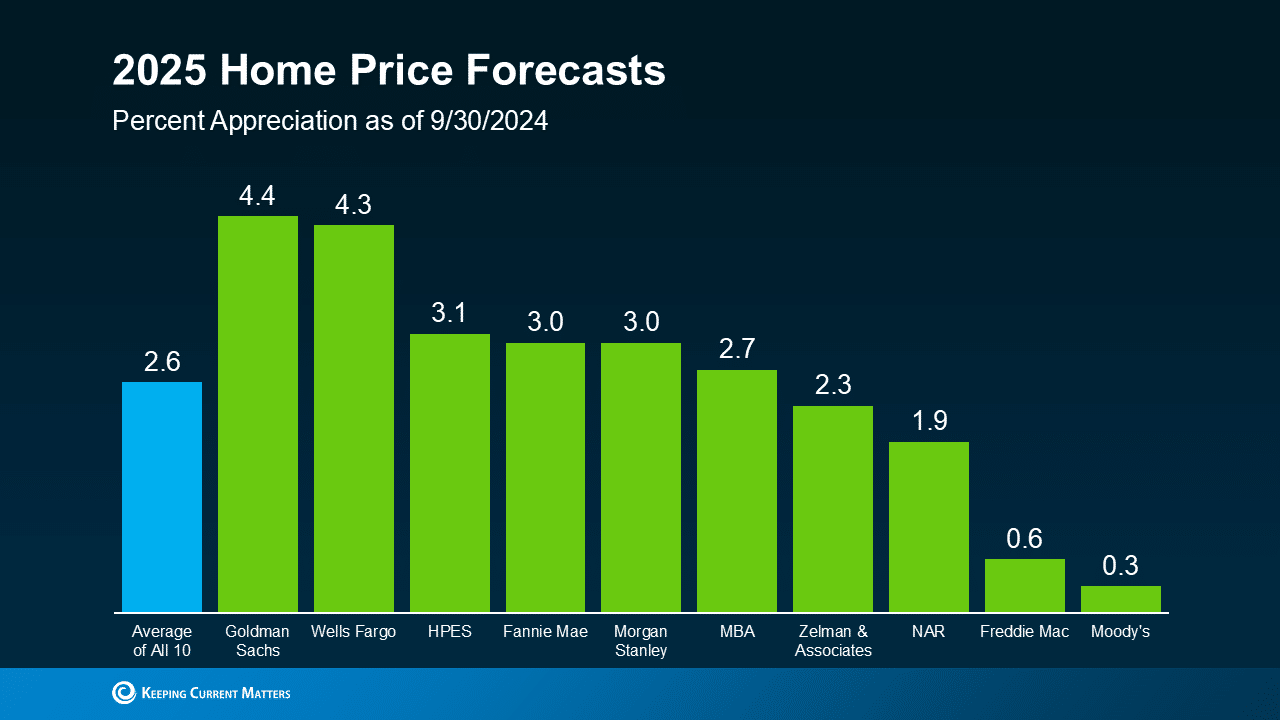

Home prices continue to appreciate. The bar chart above reflects 2025 home price forecasts from ten different industry leaders as of 9/30/2024, forecasting an average home price increase of 2.6% in 2025.

The National Association of Realtors (NAR) reported that national home prices increased 3.0% in September 2024, versus YOY September 2023. And, that marks the 15th consecutive month of year-over-year national median existing home sales price gains.

This is great news for homeowners worried about loss of recent equity gains for their current home, and also for would-be home sellers who want to capitalize on the recent price increase to leverage that gained equity for other financial priorities.

However, this is not great news for home buyers who are still struggling to find affordable housing options in today’s market.

That said, it is good to know that leading market experts are expecting the rate of home price increases to slow a bit going into 2025. But, low inventory is still causing prices to rise.

If you’re deciding whether to enter the market to purchase a home and would like to better understand your current local market, sign up to speak with a member of the Homes for Heroes team. They will answer your initial questions, and when you’re ready, connect you with our local real estate and/or mortgage specialist to begin the process.

Receive an Average of $3,000 from Homes for Heroes

Homes for Heroes assists firefighters, EMS, law enforcement, active military and veterans, healthcare workers and teachers; with buying, selling and refinancing their home or mortgage. But if you work with our local real estate and mortgage specialists to buy, sell or refinance; they also provide significant savings after you close on a home or mortgage. We refer to these savings as Hero Rewards, and the average amount received after closing on a home is $3,000, or $6,000 if you buy and sell!

Simply sign up to speak with a member of the team. There’s no obligation. After you sign up a member of our team will contact you to ask a few questions and help you determine the appropriate next steps for you.

When you’re ready, we will connect you with our local real estate and/or mortgage specialists in your area to assist you through every step of the process, and save you money when it’s all done.

It is how Homes for Heroes and our local specialists thank community heroes like you for your dedication and valuable service.

Estimate Your Savings

Learn how much you could save on your home purchase. Adjust the slider to see potential savings when you buy with a Homes for Heroes real estate and mortgage specialist. This is an estimate. Your actual savings may vary.