Wondering what is a good credit score to buy a house or refinance your mortgage? This article covers essential credit score requirements and offers valuable tips on how to manage your credit score and credit history to purchase a new home and finance it with a mortgage, or if you are looking to refinance your current mortgage.

Key Takeaways

- A good credit score for buying a house or refinancing starts at 620. That’s what a GOOD credit score starts at and goes up. Commonly, the lowest accepted credit score is 580.

- Different mortgage types have specific credit score requirements.

- Improving your credit score involves timely bill payments, managing credit card debt, and cleaning up credit report errors.

- Homes for Heroes offers significant savings when you purchase a home with their local real estate and mortgage specialists. The average amount saved is $3,000 for firefighters/EMS, law enforcement, military, healthcare professionals and teachers.

What is a good credit score to buy a house? A good credit score is typically 620 or higher, qualifying you for most common mortgage loans, and generally better interest rates, which can save you money over time. However, some mortgage lenders will finance a borrower with a credit score between 580 – 620 if that borrower meets other important financial benchmarks for pre-approval.

What is a Good Credit Score to Buy a House?

If you’re in the market to buy a house, it is valuable to know your credit score. It’s also important to learn how the minimum qualifications differ for each loan type. Here are the typical minimum credit scores for each type of mortgage loan:

- Conventional Loan: 620 or higher

- FHA 203K Loan: 620 or higher

- VA Loan: 620 or higher (some lenders will allow 580 or higher)

- USDA Loan: 640 or higher

- FHA Loan: 580 or higher (scores of 500-579 are possible but less likely)

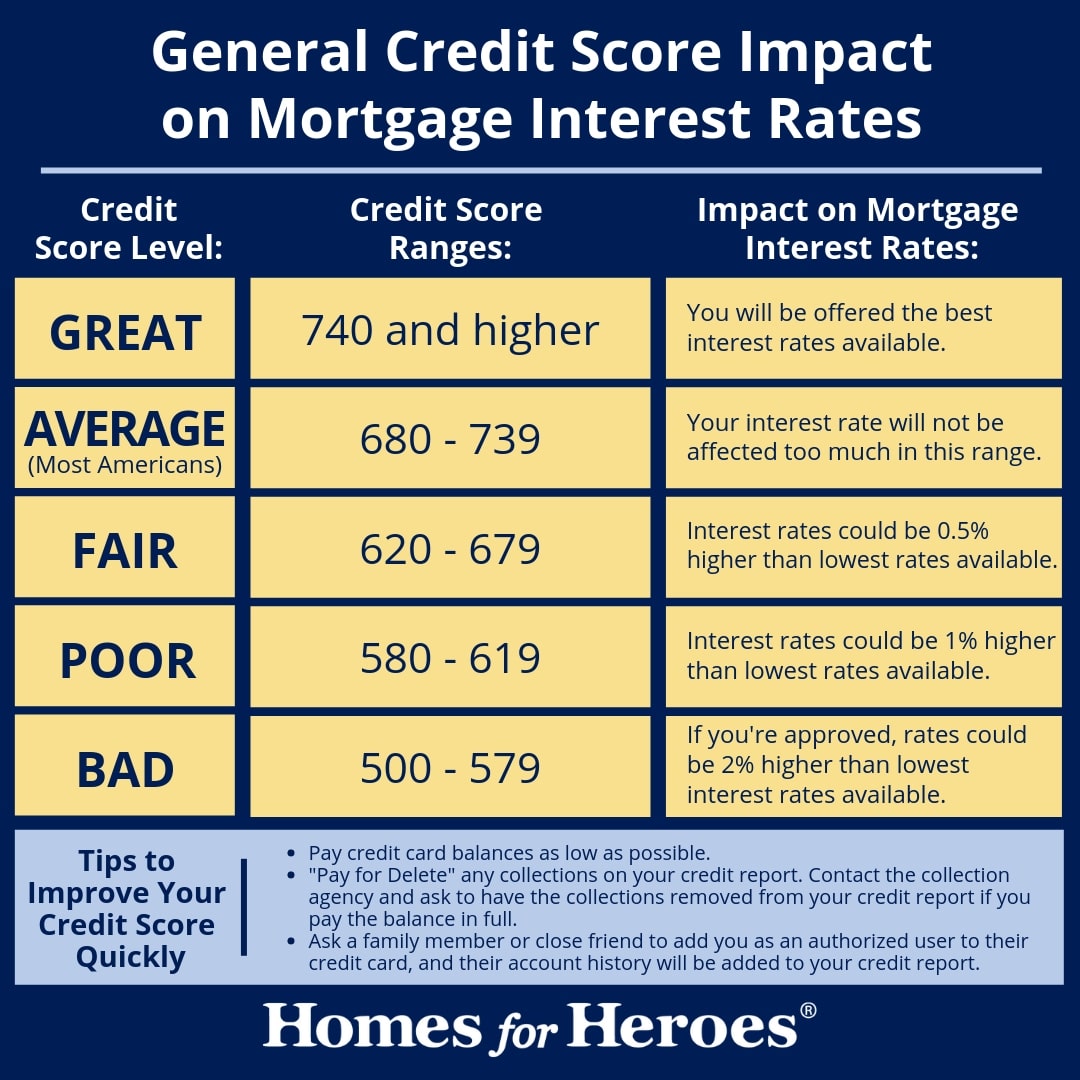

It’s important to note the credit standards listed above are generally considered the minimum for securing a home loan. The better your credit score, the better interest rate you will receive on your mortgage, saving you money in the long run. Here is the general impact of credit scores on mortgage interest rates:

But lenders don’t make decisions based on your credit score alone. In reviewing your mortgage application, they’ll also consider your income, debt, assets, employment and your ability to pay a down payment. Again, mortgage lenders are looking at the big picture, so it’s never about just one factor.

What Is a Good Credit Score to Refinance a Mortgage?

Many people choose to refinance their homes to take advantage of lower interest rates and hopefully secure lower monthly payments. Because refinancing ultimately means getting a new mortgage, you’ll need to complete many of the same steps you did when getting your first mortgage. However, the requirements for credit to refinance is a bit different. Here are the generally accepted minimum credit scores needed to refinance a mortgage:

- FHA Loan: 620 or higher

- Conventional Loan: 620 or higher

- Home Equity Loan: 680 or higher

- Cash-Out Refinance: 640 or higher

- FHA 203k Loan: 680 or higher

Although these minimum requirements are fairly standard across the industry, your individual lender may have different standards. Also, your credit score alone won’t be the only factor the lender considers when reviewing your refinancing application. They will also look at the equity you’ve built in the home, the loan-to-value ratio (LTV), your debt-to-income ratio (DTI) and more.

As with buying a house, there’s no one perfect credit score to refinance. Instead, lenders will consider your entire financial profile. If you’ve paid off much of your original mortgage, you might not need as high of a score. If you have a high DTI, you might need a higher credit score. With so many factors in play, the best thing to do is consult a mortgage specialist who can put the information together and present their findings. They will give you insight on your unique situation and how to put yourself in the best position to refinance.

Top 5 Credit Repair Tips

The truth is, unless you have a perfect credit score of 850, everyone can use these credit repair tips. Unfortunately, there’s no magic wand you can wave and instantly improve your credit score. But some of these credit repair tips are simple steps you can take to repair your credit over time. Some have almost an immediate impact, while others may take years to significantly raise your score. The important thing is all of these credit repair tips will help you build the type of credit history mortgage lenders like to see.

Here are the top five credit repair tips:

- Remove any errors or inaccuracies from your credit history report. Get your report: AnnualCreditReport.com

- Pay all of your bills on time (early is better)

- Keep your credit card debt under 30 percent of your available credit limit

- Only open a new line of credit if you intend to use it over the long-term

- Don’t close existing lines of credit, even if you don’t use them

Receive an Average of $3,000 from Homes for Heroes

Homes for Heroes assists firefighters, EMS, law enforcement, active military and veterans, healthcare workers and teachers; buy, sell and refinance their home or mortgage. But if you work with their local real estate and mortgage specialists to buy, sell or refinance; they also provide significant savings after you close on a home or mortgage. They refer to these savings as Hero Rewards, and the average amount received after closing on a home is $3,000, or $6,000 if you buy and sell!

Simply sign up to speak with a member of the team. There’s no obligation. After you sign up they will contact you to ask a few questions and help you determine the appropriate next steps for you. When you’re ready, they will connect you with their local real estate and/or mortgage specialists in your area to assist you through every step, and save you money when it’s all done.

It is how Homes for Heroes and their local specialists thank community heroes for their dedicated and valuable service.

Estimate Your Savings

Learn how much you could save on your home purchase. Adjust the slider to see potential savings when you buy with a Homes for Heroes real estate and mortgage specialist. This is an estimate. Your actual savings may vary.